Snowflake

See partnership

Your audio file will ready in a few seconds...

TL;DR: We created five graphs to give a better understanding of why financial inclusion is relevant. Each graph explores topics such as bank account ownership, debit card ownership, savings, access to Internet and mobile banking, and having a minimum wage job.

Financial inclusion is not an abstract concept. As we mentioned in a previous blog post, there is a strong relationship between accessibility to banking services and gender equality. Societies would reach more equality and prosperity if women and female bodies have equal access to financial services.

1.1 billion of the world’s underbanked adults are women. They also tend to be excluded from the financial system at higher rates than their male counterparts. Despite collective efforts to bridge financial inclusion, the gender gap has remained unaltered since 2011.

Using disaggregated data, we created a series of charts for a better picture of the global panorama. We selected five financial inclusion indicators considered key by the Group of Twenty (G20) and generated each chart with data from the World Bank and the Global Findex Database.

The Global Findex Database presents information by country and by region. Because we’re interested in providing an overview of the global situation, the information is organized in seven regions:

The information in each graph is in abbreviated form.

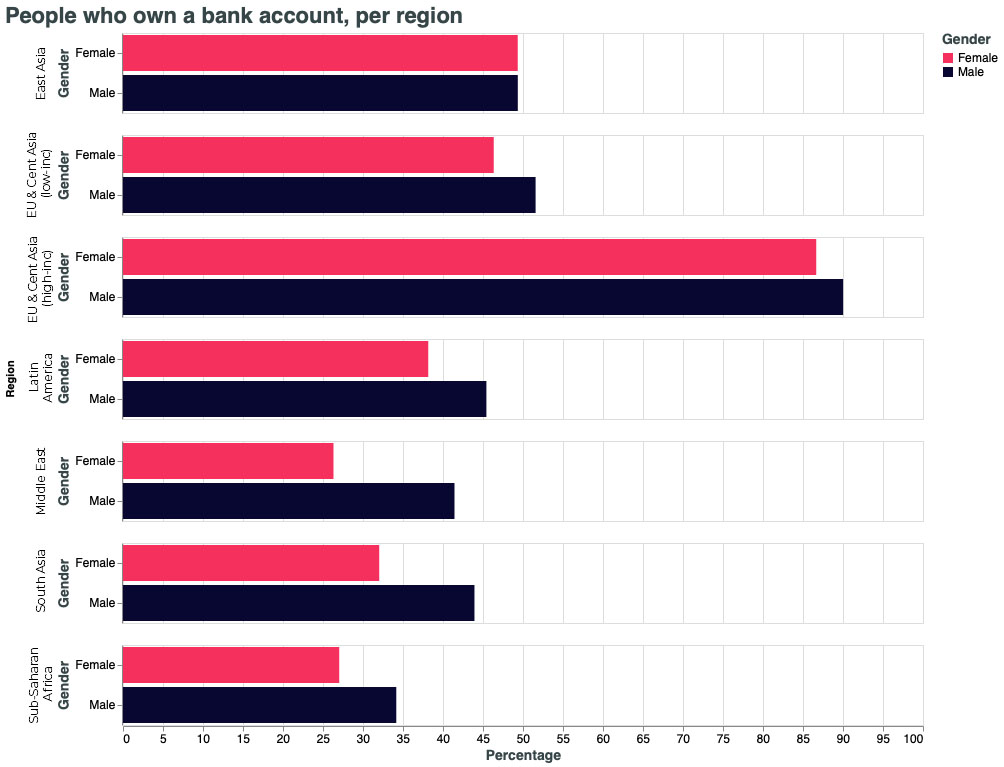

The first graph shows the percentage of the total population that owns a bank account.

In European high-income countries, for instance, more than 85% of the population use banking services.

The difference between men and women in regions like Europe or East Asia is not as pronounced as in the Middle East or South Asia.

In the latter regions, cultural and social factors play an important role in women having access to a bank account.

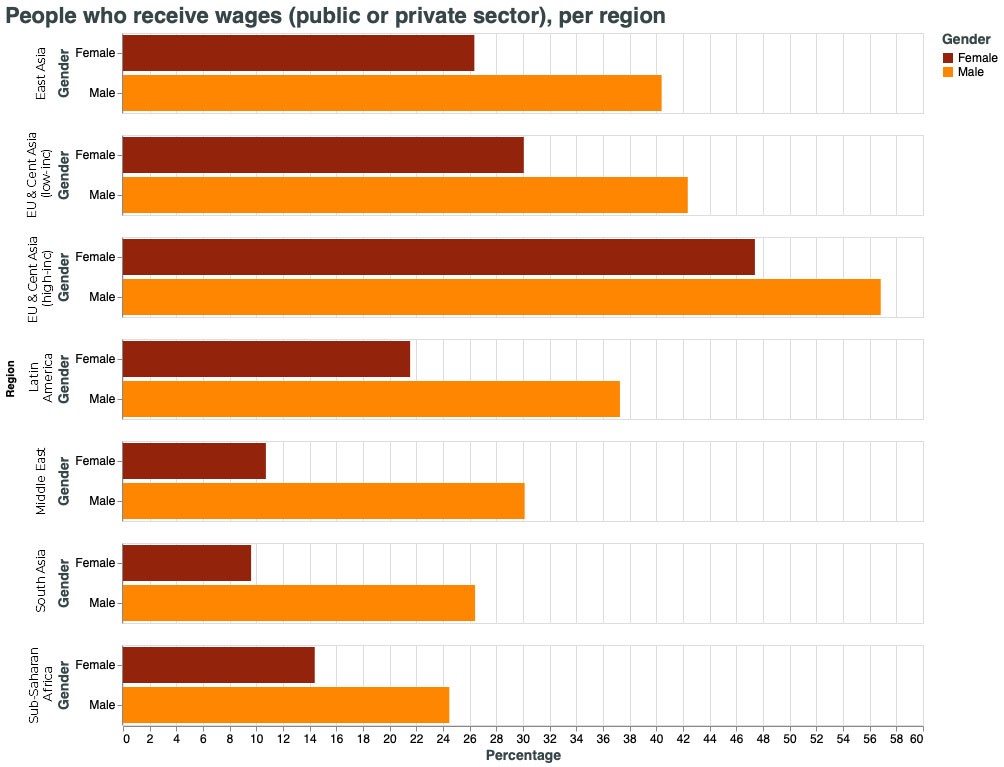

Receiving a wage is an important indicator of financial stability and, therefore, also of inclusion. Nevertheless, especially in the Global South, women are considerably at odds in this category.

What does this mean?

In many cases, not receiving a wage implies either depending on an income (for example, a spouse or family member) or having an informal source of income.

In conclusion, the situation puts women at a disadvantage. It limits their access to insurance, healthcare, and puts them at risk of precarious employment.

Having a working wage and owning a bank account makes a significant difference in people’s lives.

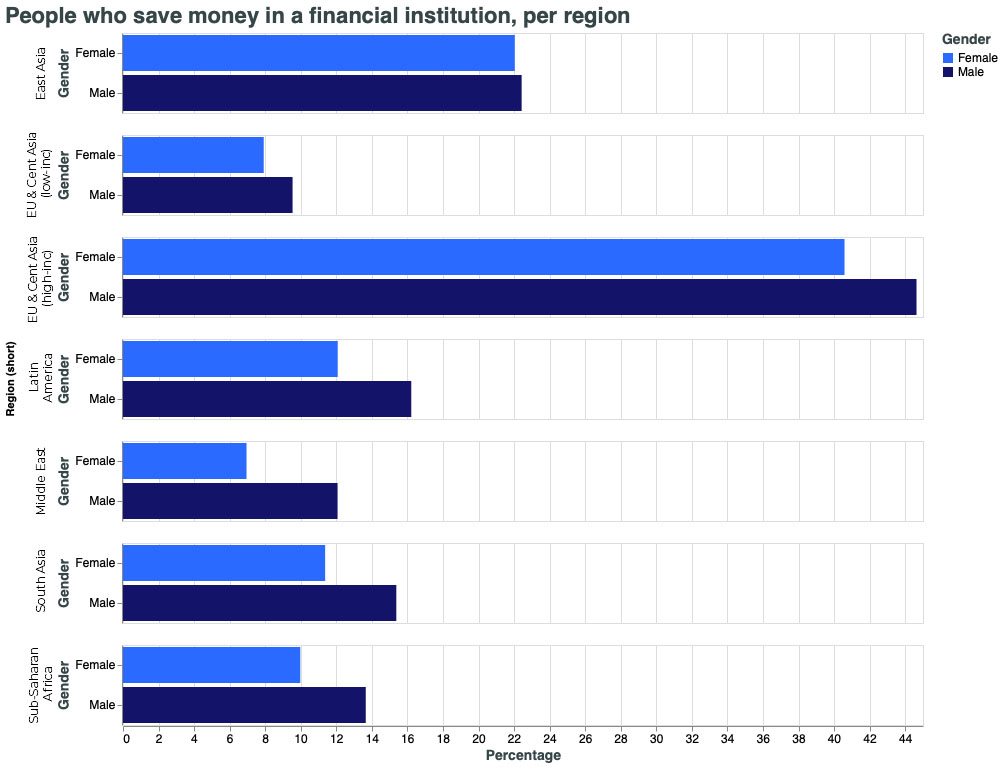

This third chart stems from the previous two. Working allows people to save money for whatever goals they have. However, because men around the world have a greater saving capacity than women, the highlighted inequalities increase.

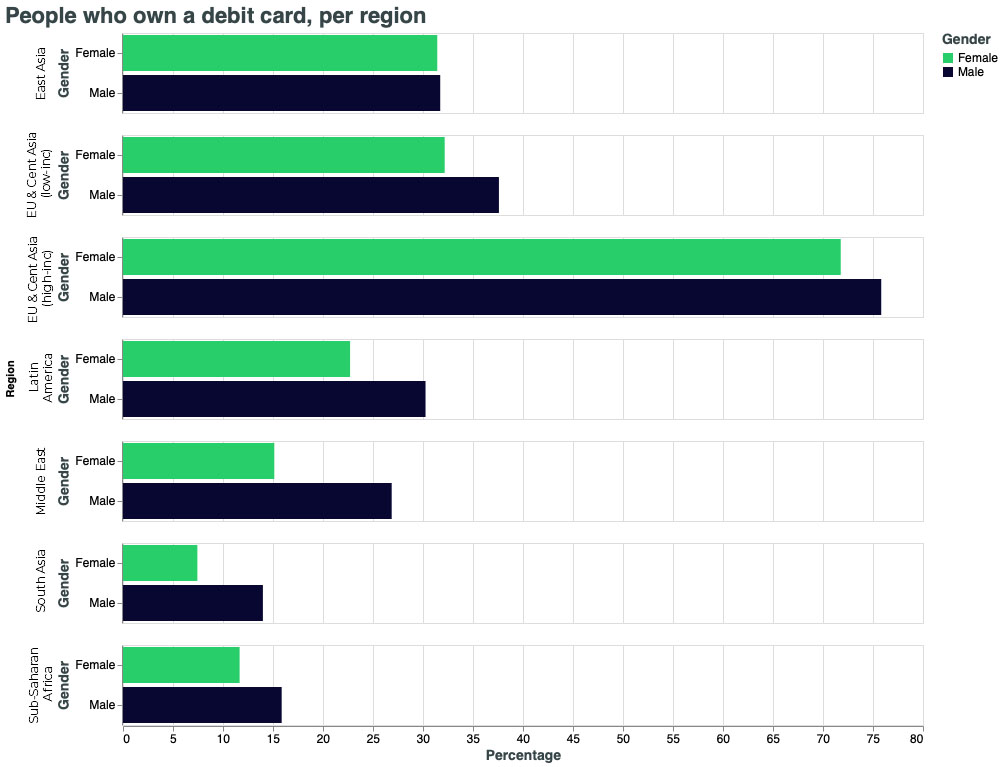

Owning a debit card can provide users incredible financial freedom.

However, as owning a debit card is linked to owning a personal bank account, every region behaves similarly to the first graph.

In the case of Sub-Saharan Africa and South Asia, for instance, the percentage of women who own a debit card is less than 10%.

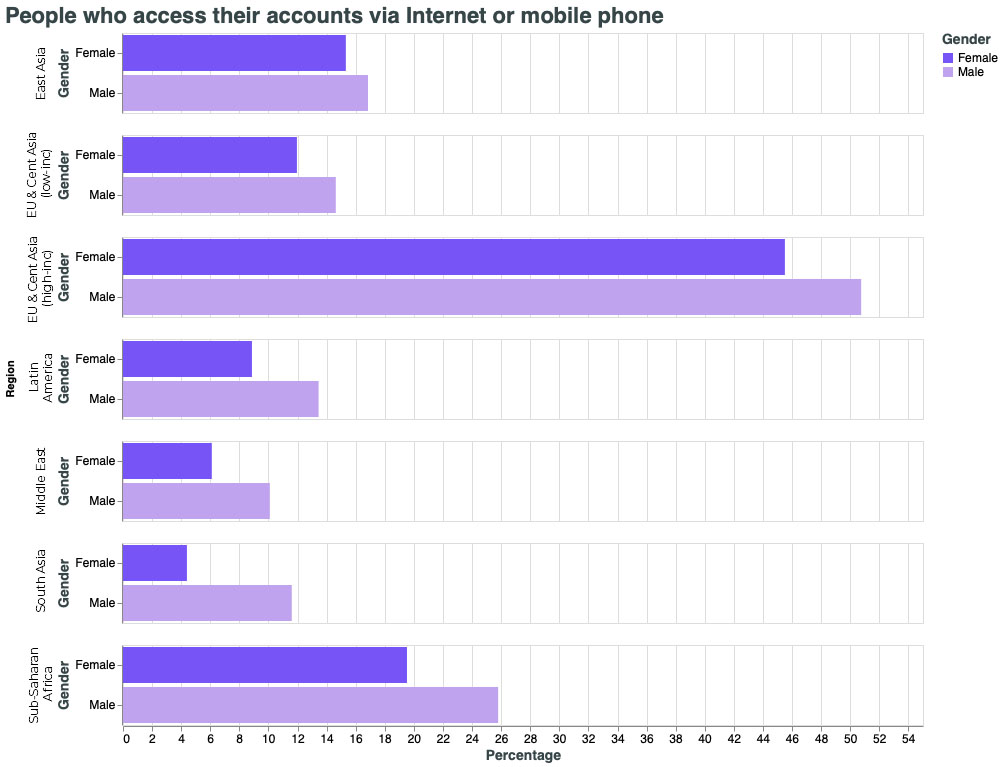

Internet access proves very useful for people who live in remote areas and need to use specific banking services.

Because Internet access helps reach a greater number of people, governments around the world have created programs to bridge the digital divide. Aided by technology, they aim at ensuring financial inclusion for everyone.

The five graphs together show how, even in developed nations, women are consistently underbanked, underpaid, and excluded from important digital services.

Although the Covid-19 pandemic has dramatically improved digital and financial inclusion, the challenges to bridge such gaps require a collective effort from private and public institutions around the world.

Therefore, providing female-exclusive banking options that make it easier for informally sourced parties to access financial services is one way financial inclusion can help reshape the future in ways that ensure gender parity.

Was this article insightful? Then don’t forget to look at other blog posts and follow us on LinkedIn, Twitter, Facebook, and Instagram.